5 Reasons China’s Recent Stock Market Rally is Fundamentally Different

By Brendan Ahern, KraneShares CIO

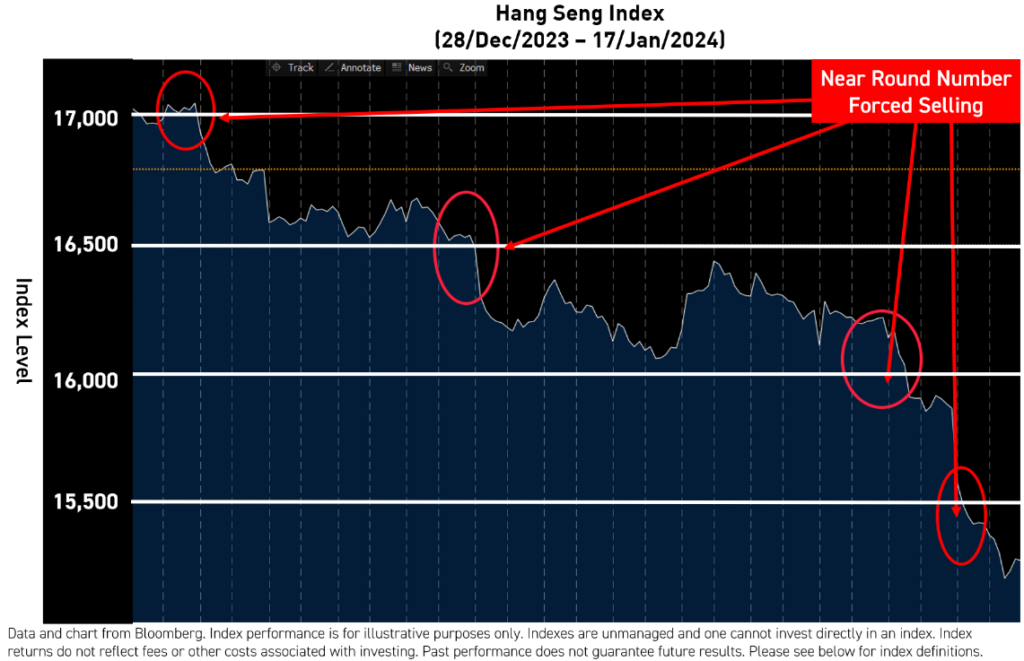

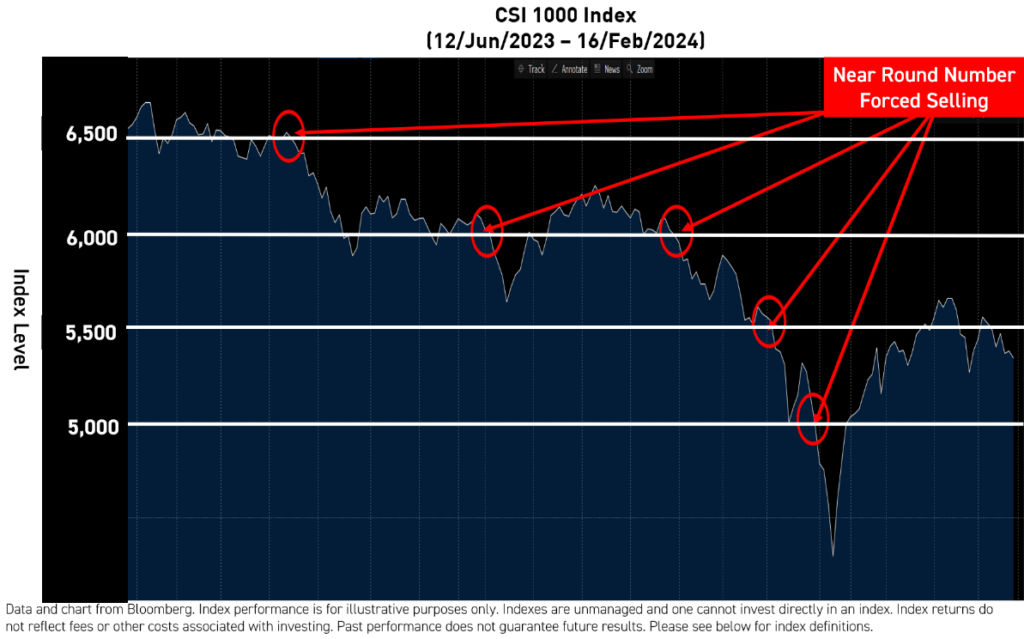

So far, 2024 has been a dynamic year for China’s equity markets. In January, a derivative-induced meltdown sent Chinese stocks lower on the Shanghai and Shenzhen Stock Exchanges, spilling over to Hong Kong and US-listed China ADRs. This liquidation event was set in motion by low China equity positioning among investors. As Hong Kong and Mainland China benchmarks hit significant, round number index levels, they triggered the liquidation of index futures. With no buyer to take the other side of the trade, markets fell.

But things may be looking up for China’s stocks. Since 2nd February and through the end of April, the KraneShares CSI China Internet UCITS ETF (Ticker: KWEB) has returned +21.30% and the KraneShares ICBCCS S&P China 500 UCITS ETF (Ticker: CHIN) has returned +15.52% versus the S&P 500's 1.90% and the Nasdaq 100's -0.95%.1 Can this rally sustain itself? We have compiled five key points for investors to consider as to why this breakout may be fundamentally different from previous rallies.

The performance data quoted represents past performance. Past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed or sold, may be worth more or less than the original cost. Current performance may be lower or higher than the performance quoted. For performance data current to the last month-end, please click here for KWEB and here for CHIN.

1. The government is buying stocks and talking about it.

China's government is buying Mainland stocks to stabilize the domestic stock market and influence stock market indices. Mainland China lacks market circuit breakers, which are temporary measures that halt trading to curb automatic selling on stock exchanges. These circuit breakers are common in many developed markets, including the US. Since China does not have a circuit breaker, during periods of volatility, government-related entities will act as buyers of last resort. In the past, government buying was done discretely without much publicity, this time China is being much more public with its stock purchases.

One such buyer is Central Huijin Investments, an entity within China's sovereign wealth fund. The state-linked entity announced purchases of Mainland China-listed ETFs in February2 and subsequently increased its holdings of Mainland bank stocks in April, according to its quarterly reports3.

State-linked stock buyers are common in Asian markets and their activity can shore up investor confidence. Japan’s central bank, for example, has a long history of buying stocks and ETFs listed on Japanese exchanges. We believe one reason Asian investors are overweight Japanese stocks is due to the government's purchase of equity ETFs and, more recently, corporate reforms viewed as shareholder friendly. This similar recipe of equity investing success is being replicated in China as state-linked funds buy Mainland -listed mega-cap stocks and ETFs that, in turn, influence the stock indices.

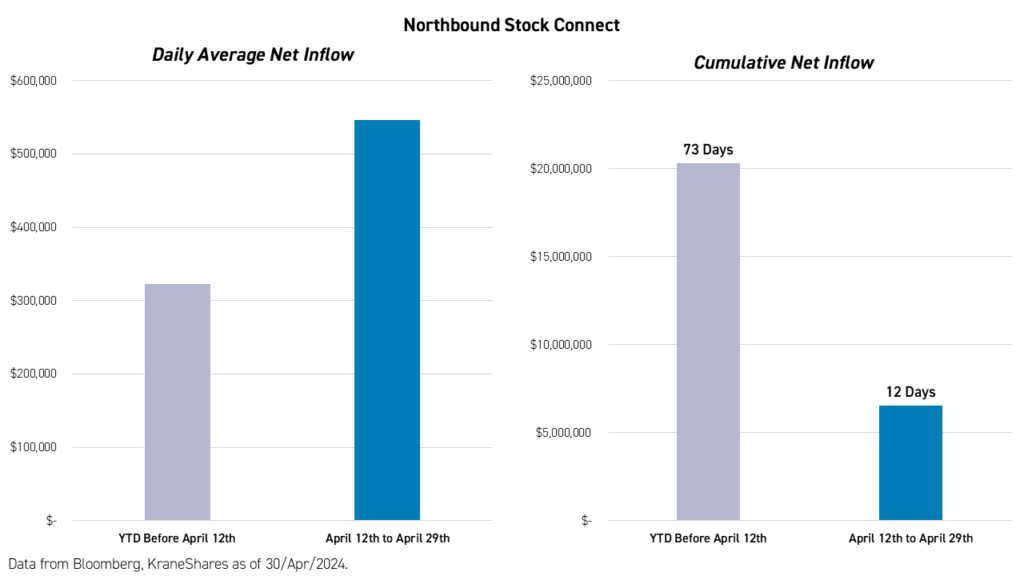

State-linked buyers are partially funding their purchases through Northbound Stock Connect, a mutual market access program that allows investors to purchase shares listed on the Shanghai and Shenzhen stock exchanges through accounts in Hong Kong. The surge in Northbound Stock Connect inflows in recent weeks is striking.

2. Global investors are returning.

January's fall was partly due to investors' neutral or under-weights to Chinese equities. US investors were among the first to shed their China positions due to the Trade and Technology Wars, followed by China’s internet regulatory cycle and zero COVID policy. Next, European investors trimmed their positions after the geopolitical uncertainty that unfolded following Russia’s invasion of Ukraine. Asian investors eventually followed suit, though they were slower to reduce their exposure due to their proximity to China's economic orbit. Finally, local Chinese investors divested from Mainland stocks much later, following the derivative-induced selloff earlier this year.

We suspect re-allocations to China’s equity market could occur in the opposite order as local Chinese investors return first, followed by Asian investors and then European and American investors.

Southbound Stock Connect (the mutual market access program that permits Mainland investors to invest in Hong Kong-listed stocks) flows from Mainland China into Hong Kong stocks show that local Chinese investors have already started to return, at least to offshore stocks.

At the same time, we believe many Asia-focused investors who have been overweight India and Japan are growing concerned about India's high valuations and Japan's continued currency weakness. China’s equity market could be a beneficiary of investors moving profits from high-valuation markets to low-valuation markets.

3. New policy supports shareholders.

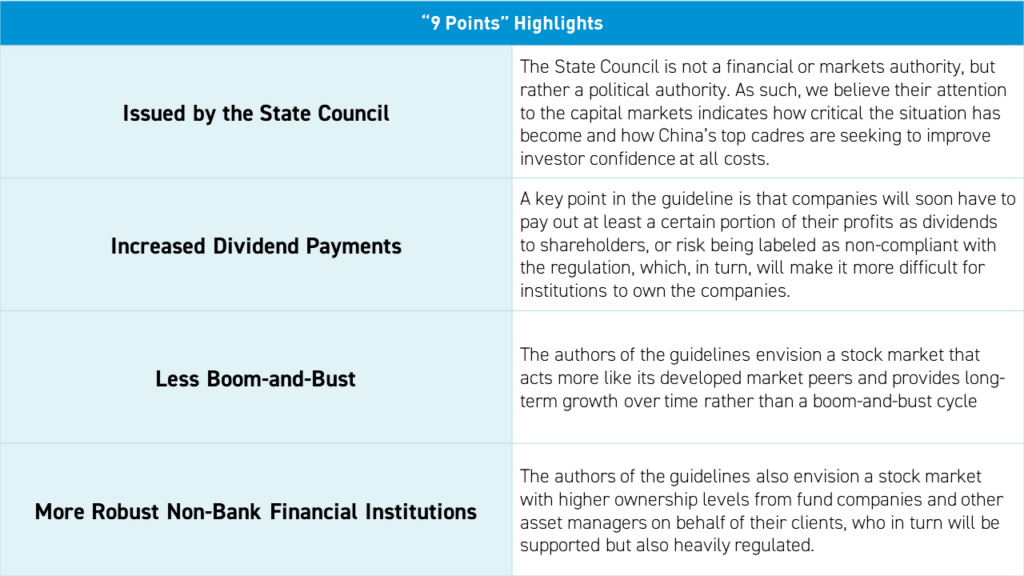

On April 12, The State Council issued "9 Key Points" to improve China's capital markets, a rare document to come out of the State Council, China’s top political body (like the President’s cabinet in the US), which usually does not comment on markets. Among the measures are initiatives to control the supply of IPOs, encourage companies to pay dividends and improve their corporate governance, and promote bank and trust products to allocate more to equities.

4. The consumer is alive and the economy is improving.

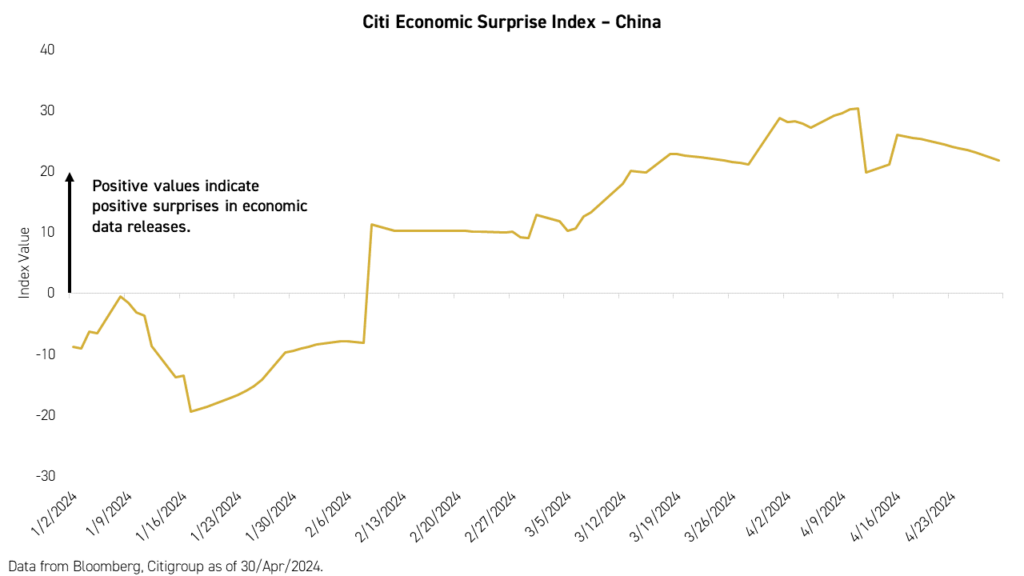

China's economic cycle is improving, as evidenced by Q1 2024 GDP, which came in at 5.3% versus an estimated 4.8%, representing an improvement of +1.6% compared to Q4 2023.4 The Citi Economic Surprise Index measures the degree to which economic releases in a given country surprise to the upside or downside. The China index has moved up steadily since the start of the year after declining in 2023. Although expectations for these releases were already low, the index indicates a general upward trend starting in January.

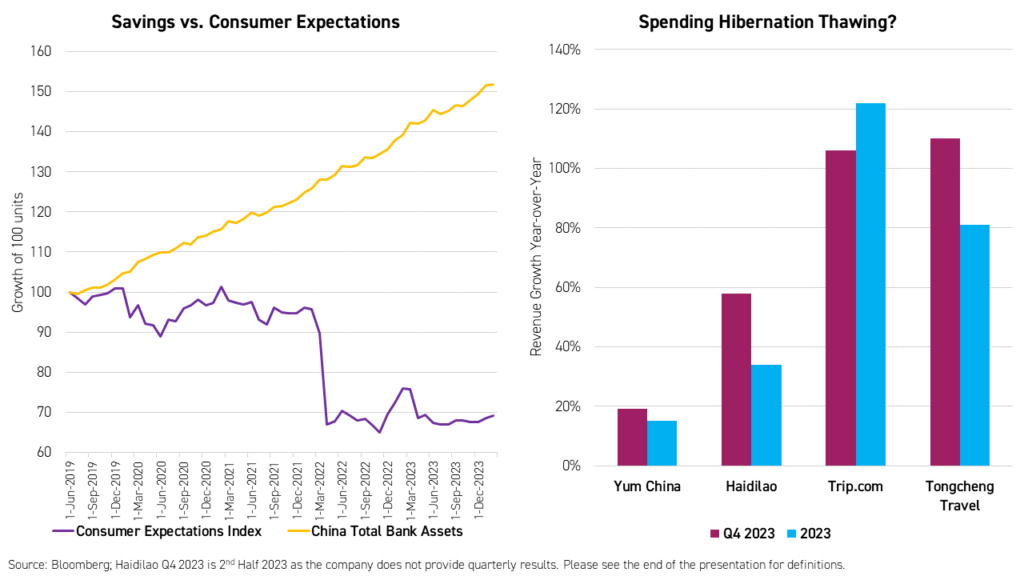

Consumer confidence is slowly improving, though Chinese households maintain their high historical savings rate. Unleashing these savings would likely produce a significant economic boost.

Consumption is rebounding, but it continues to be concentrated in services such as travel, which was reflected in the Q4 2023 financial results from restaurant chains and travel agencies. If you were going to start to spend, what would you do first? Personally, I would take my wife out to dinner. Then, I'd plan a vacation.

Fliggy, Alibaba's online travel platform, reported that "outbound travel bookings during the holiday in 2024 doubled year-on-year".5 International travel costs more than domestic travel and popular destinations include Japan, Thailand, South Korea, and Australia. This could indicate an increased willingness to spend compared to 2023, when travel was more concentrated domestically.

Policy support for consumption has been incremental, though support is starting to accelerate. Following the “Two Sessions” in March, the government announced increased incentives for the upgrading of large items such as automobiles and home appliances.4 This indicates the government's keen interest in seeing the economy recover.

5. Present valuations cannot be ignored, and buybacks are surging.

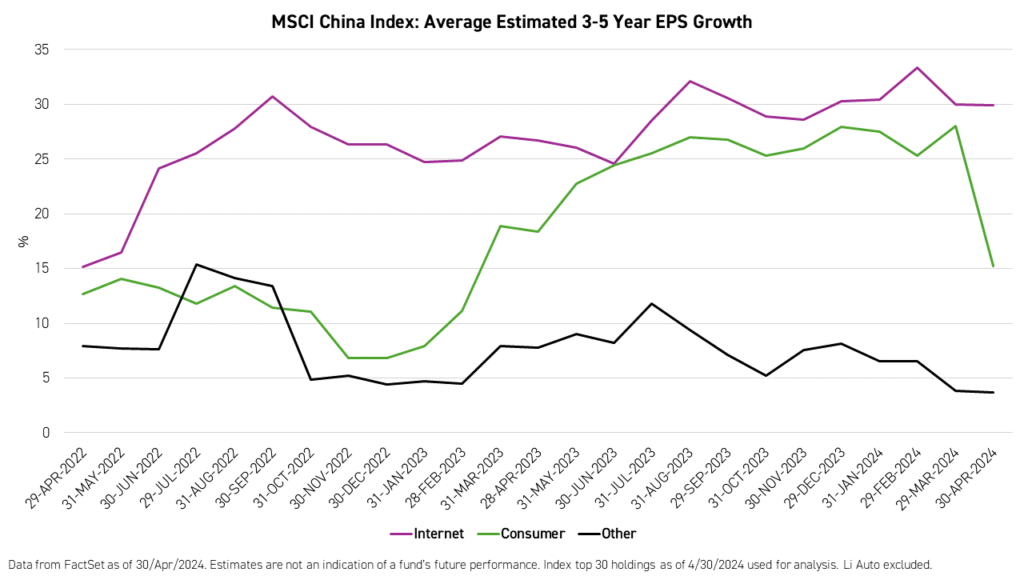

Low valuations paired with improving earnings could be a catalyst for continued outperformance in certain sectors in China. Although some investors have yet to recognize the attractive valuations in China equities, many companies are taking the matter into their own hands by buying back their stock, mostly in the internet sector.

At the same time, the fundamentals for these companies are also improving. The 3 and 5-year earnings per share (EPS) growth estimates for the internet and E-Commerce companies within the MSCI China Index have been upward trending over the past two years and are currently multiples higher than broad consumer stocks and the average for other industries within the index.

Conclusion

The potential for the current China rally to continue depends on several factors and we believe many of those factors are already in place. The current rally could be fundamentally different because state-linked investors are actively promoting their stock purchases, global investors are returning, albeit slowly, shareholders are being supported by top-down policies, the economy is recovering meaningfully, and valuations are more attractive than ever with improving earnings expectations for internet companies.

Investors can access both onshore and offshore China stocks through the KraneShares ICBCCS S&P China 500 UCITS ETF (Ticker: CHIN). For offshore China shares (Hong Kong and US-listed stocks), we prefer top internet companies, which can be accessed through the KraneShares CSI China Internet UCITS ETF (Ticker: KWEB).

This is a marketing communication. Please refer to the prospectus of the UCITS, the KIID, and the PRIIPs before making any final investment decisions.

Citations:

- Data from Bloomberg as of 30/Apr/2024.

- Global Times. “Central Huijin Investment Co increases holdings in China’s A-shares market ETFs,” Global Times. 6th February, 2024.

- “China state fund pours $41 bln into stock market in Q1, reports show,” Reuters. April 22, 2024.

- Data from Bloomberg as of 31/Mar/2024.

- Data from Alibaba as of 30/Apr/2024.

Definitions:

Consumer Expectations Index: Consumer confidence is a measure of the willingness of consumers to part with their cash in exchange for goods and services. The metric is usually gathered by analyzing spending trends among individuals in an economy and is usually maintained by a government agency responsible for surveys and economic data.

Hang Seng Index: The Hang Seng Index ("HSI"), the most widely quoted gauge of the Hong Kong stock market, includes the largest and most liquid stocks listed on the Main Board of the Stock Exchange of Hong Kong. The index was launched on November 24, 1969.

CSI 1000 Index: The CSI 1000 Index selects 1000 small cap securities with good liquidity in A shares that are not included in CSI 800 Index. The index was launched with a base value of 1000 and a base date of December 31, 2004.

MSCI China Index: The MSCI China Index captures large and mid-cap representation across China A shares, H shares, B shares, Red chips, P chips and foreign listings (e.g. ADRs). With 703 constituents, the index covers about 85% of this China equity universe. Currently, the index includes Large Cap A and Mid-Cap A-shares represented at 20% of their free float adjusted market capitalization. The index was launched on October 31, 1995.

Earnings per Share (EPS): Earnings per share is a company's net income subtracted by preferred dividends and then divided by the average number of common shares outstanding.

Share Buyback Yield: The value of the outstanding purchases in a company's current share repurchase plan as a percentage of the company's current free-float market capitalization.