KWEB China Internet Market Volatility FAQ

We believe China's internet industry presents one of the most compelling long-term growth opportunities for investors today. However, given that our KraneShares CSI China Internet UCITS ETF (ticker: KWEB) targets a single sector and companies based in China, it tends to have greater volatility than broader categories or developed market investments. To help potential investors make more informed decisions, we have compiled the following responses to the top frequently asked questions we receive from our clients. Additionally, we provide daily market updates through our blog China Last Night. Please click here to subscribe.

How might KWEB be affected by the Holding Foreign Companies Accountable Act?

Congress passed the Holding Foreign Companies Accountable Act (HFCAA) in December of 2020. The new law requires all US-listed foreign companies to allow the Public Company Accounting Oversight Board (PCAOB) to inspect their audit books, disclose government ownership, if any, or face delisting. The law only applies to listed stocks, not ETFs, so KWEB is not at risk of being delisted under this law.

On December 15th, 2022, auditors from the Public Company Accounting Oversight Board (PCAOB) gained complete access to inspect and investigate auditors in Hong Kong and Mainland China.1 We believe this historic development significantly reduced the delisting risk for US-listed Chinese stocks. In light of this development, KWEB has suspended conversions of American depositary receipts (ADRs) into Hong Kong-listed shares.

What are the potential benefits to companies listing in Hong Kong?

There are many potential advantages to having a Hong Kong listing, even if a company is already listed in the US or elsewhere. US and Hong Kong share classes are fungible, meaning shares can be freely converted from one listing location to another, as long as your broker allows for such a conversion. KraneShares' professional management team handles the conversion of US-listed stocks into Hong Kong shares for KWEB's holdings on behalf of our clients.

One key benefit of having a dual primary or primary listing in Hong Kong is that having such a listing enables Mainland Chinese investors to access these stocks, often for the first time, via Southbound Stock Connect. This could mean significant inflows to companies including Alibaba, which announced their intention to make their Hong Kong listing a dual primary listing in late July 2022. For reference, Tencent is primarily listed in Hong Kong and accessible to Mainland investors via Southbound Stock Connect. As of February 13, 2023, Mainland investors held 9.3% of Tencent's shares outstanding.4

How do US-China relations affect KWEB?

Headline news surrounding the US-China relationship can negatively impact investor sentiment around KWEB and its underlying holdings, injecting volatility into the China internet space. However, the revenues of KWEB companies are mostly derived from China's consumer economy and do not depend on trade with the US.

Since the end of last year, US-China relations have improved markedly. As well-known China political scholar Jessica Chen Weiss said at our conference in November 2022, both countries are likely to create a breathing space and take tentative steps toward creating what Weiss called a “floor” for US-China tensions this year. Nonetheless, progress was stalled in February when an unidentified balloon vessel, having originated in China, was detected in US airspace. As a result of this incident, US Secretary of State Antony Blinken postponed his scheduled trip to Beijing.

It is important to note that Antony Blinken’s visit to China has only been postponed, not cancelled. Furthermore, Treasury Secretary Janet Yellen is still scheduled to visit China this year to confer with her Chinese counterparts.

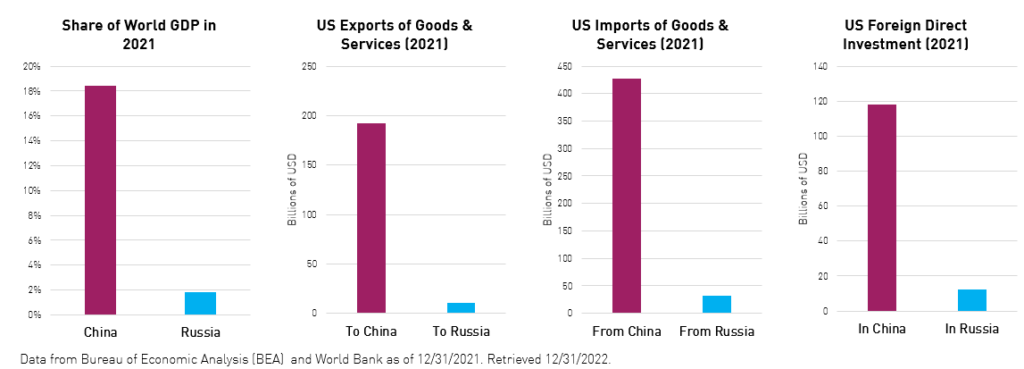

Could China be vulnerable to similar geopolitical risks as Russia?

No. China and Russia are very different from one another economically, culturally, and geographically.

China is an integral part of the global economy, accounting for a far larger share of global GDP, US imports/exports, and US foreign direct investment. China accounted for over 18% of global GDP in 2021 while Russia only accounted for less than 2%. Meanwhile, the US imported over $400 billion worth of goods and services from China in 2021 and less than $50 billion worth from Russia, mostly oil and gas.

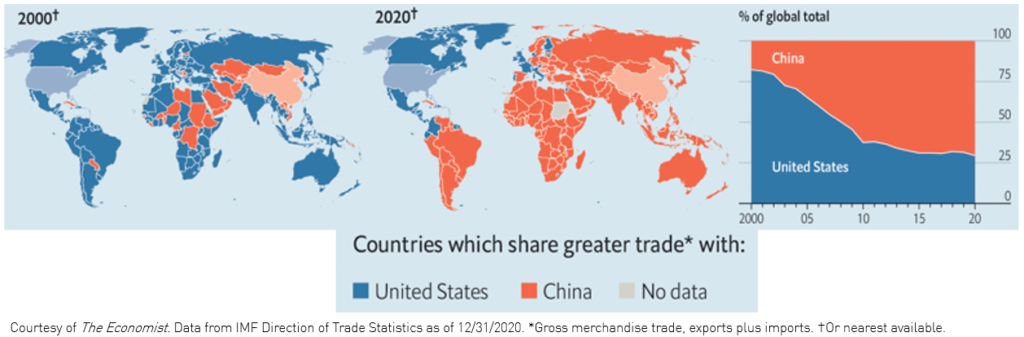

As the world’s largest trading partner, ensuring that global trade is stable and healthy is a top priority for China. Freezing trade with China could potentially cause a global depression, not just a bout of market volatility.

The US and China have too much to lose to fully decouple from one another. As such, we believe the risk that similar economic sanctions are applied to China is low. On March 25th, 2022, US Treasury Secretary Janet Yellen told CNBC that she does not believe that sanctions on China are “necessary or appropriate.”2

Despite its neutral official stance, China has expressed its disapproval of the invasion through various soft power measures. China state-backed banks, including the mammoth Asian Infrastructure Investment Bank (AIIB), have suspended Russian activity. Meanwhile, China has urged “constraint” from all parties through multilateral channels.

What are some potential near-term catalysts for KWEB?

- China is currently easing monetary conditions while most of the developed world is tightening. While the cost of capital for US internet firms is rising, the cost of capital for KWEB companies is falling.5

- China’s government seeks to achieve an ambitious 2023 GDP Growth target of over 5% and dramatically reduce unemployment.3 China’s internet giants will play an integral role in achieving these goals.

- KWEB’s long-term growth story remains intact. China’s internet population continues to grow, and China’s internet companies continue to grow their revenues.6

- The continued beneficial impact of China's reopening on the revenues of China's E-Commerce and internet-related industries, the transmission engines of China's consumer economy.

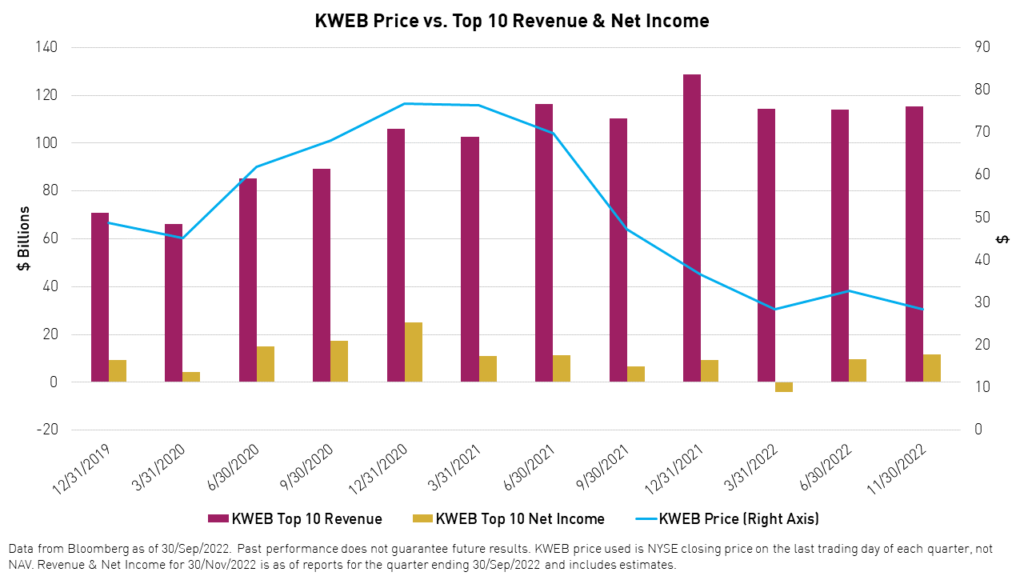

What about KWEB's fundamentals?

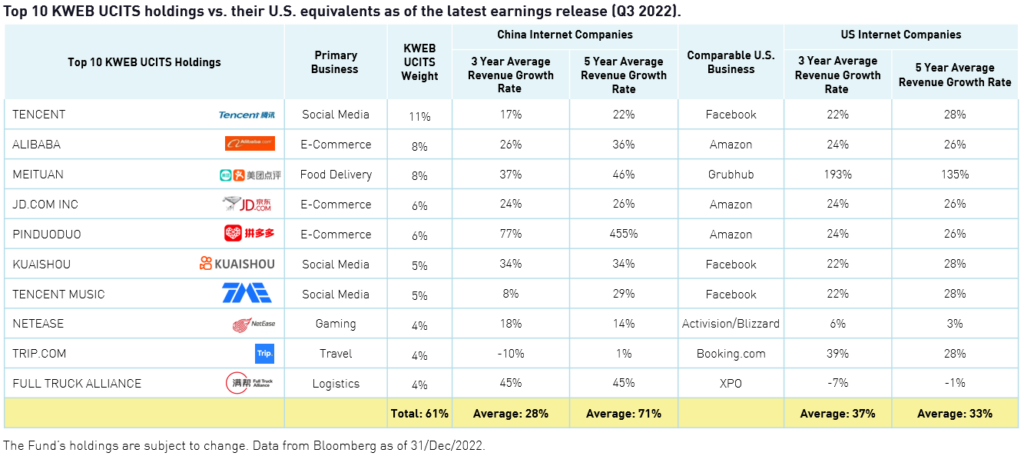

- The 3 & 5-year average revenue growth rates for China internet companies are similar to those of many U.S. internet companies.

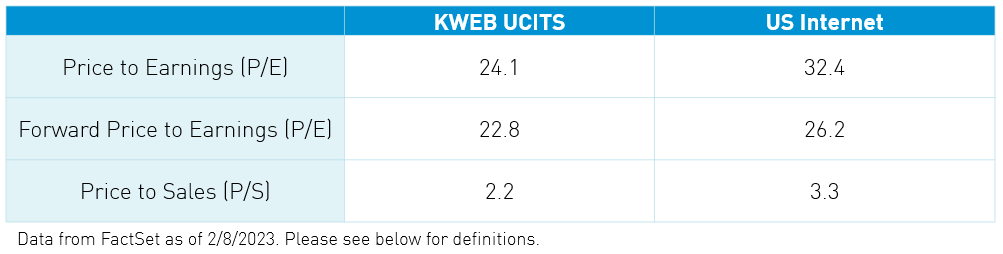

- However, companies in KWEB continue to trade at, on average, 30% lower multiples versus their US peers.

- We believe that most of the price action in KWEB over the past 18 months has not been fundamentally driven.

Citations

- Williams, Erica Y. “PCAOB Secures Complete Access to Inspect, Investigate, Chinese Firms for First Time in History,” Public Company Accounting Oversight Board (PCAOB) News Release. December 15, 2022.

- Franck, Thomas. “Treasury Secretary Yellen sees no need for China sanctions as US tries to deter aid to Russia,” CNBC. March 25, 2022.

- Release From the People's Republic of China, National Party Congress (NPC) dated October, 2022.

- Data from Hong Kong Exchanges & Clearing as of 2/13/2023.

- Based on US and China interest rate differential. Data from Bloomberg as of 1/31/2023.

- Data from Bloomberg as of the latest earnings releases for KWEB constituents (9/30/2022).

Definitions

Definitions:

Dow Jones US internet Composite Index ("US Internet"): The Dow Jones Internet Composite Index is designed to measure the performance of the 40 largest and most actively traded stocks of U.S. companies in the internet industry. To be eligible for the index, a company must derive at least 50% of cash flows from the internet. The index was launched on February 18, 1999.

CSI Overseas China Internet Index: CSI Overseas China Internet Index selects overseas listed Chinese Internet companies as the index constituents; the index is weighted by free float market cap. The index can measure the overall performance of overseas listed Chinese Internet companies. The Index is within the scope of the IOSCO Assurance Report as at 30 September 2018. The index was launched on September 20, 2011.

Price to Earnings: The price-to-earnings ratio (P/E ratio) is the ratio for valuing a company that measures its current share price relative to its per-share earnings (EPS). The price-to-earnings ratio is also sometimes known as the price multiple or the earnings multiple.

Forward Price to Earnings: Forward price-to-earnings (forward P/E) is a version of the ratio of price-to-earnings (P/E) that uses forecasted earnings for the P/E calculation. While the earnings used in this formula are just an estimate and not as reliable as current or historical earnings data, there is still benefit in estimated P/E analysis.

Price to Sales: The price-to-sales ratio is a valuation ratio that compares a company’s stock price to its revenues. It is an indicator of the value that financial markets have placed on each dollar of a company’s sales or revenues.