China Internet Regulations: Where We’ve Been and What’s Next

Subscribe to China Last Night, our daily note on China’s capital markets.

During times of market volatility, we keep our readers informed on the latest updates from China

Read our latest post

Executive Summary

- A new timeline from China’s Ministry of Industry and Information Technology1 could set a finish line for regulatory uncertainty within the China internet sector.

- Supporting the development of the digital economy is still a key policy priority for China. Broader regulations on the internet sector are similar to the E.U.'s General Data Protection Regulation (GDPR) and other measures that have been proposed in the United States.

- While new regulations regarding after school tutoring programs sparked a broader selloff, they are not applicable to the China internet sector as a whole.

- Recent reforms in the internet sector parallel reforms to China’s health care sector in 2018, which served as a growth driver for health care companies in the following years.

- KraneShares’ CIO Brendan Ahern will conduct a live Q&A to help address investors’ questions after this week’s volatility. He will also provide an overview of where we’ve been and what’s next for China’s markets.

China Market Volatility Update and Q&A With KraneShares CIO Brendan Ahern – Tuesday, August 3rd, 11:00 am – 12:00 pm EDT. Register Here

In China, 30% of all retail sales flow through internet companies2. These companies have quickly reshaped China’s economy and are vitally important to its success. Yet, much like in the U.S. and globally, regulation has not kept pace with the growth of internet platforms. The entire world is now more concerned about data security, privacy, and monopolistic behavior from internet conglomerates. Therefore, we should not be surprised that China has decided to address these issues at home. The way China’s regulations were announced has led to uncertainty and hurt stock performance, but a clearer roadmap for reform is materializing, which may help to shore up markets.

Internet Review Timeline & Future Regulations

The Ministry of Industry and Information Technology (MIIT) announced that a six-month review of internet companies commenced on July 23. The review will encompass cybersecurity, data privacy, consumer protection, and monopolistic behavior1. We believe the MIIT announcement outlines a potential finish line for regulatory uncertainty, which is positive for markets. According to the MIIT, “up to now, 68 leading Internet companies including Baidu, Alibaba, Tencent, ByteDance, Sina Weibo, and iQiyi have completed rectification as required.”3

Last quarter, Alibaba received a multi-billion dollar fine for anti-competitive practices. Ant Group has already successfully restructured as a financial holding company subject to bank rules. Meituan is taking steps to ensure its drivers make at least the local minimum wage while improving their training and safety conditions. Tencent has given up exclusive rights to certain content on its music streaming services. Didi, whose rushed IPO cratered post-regulation announcement, likely still faces a steep pending fine (Didi is not currently held in any KraneShares ETFs).

For a broader picture of the scope of future regulations, the government laid out a “Common Prosperity” strategy consisting of four pillars of prosperity it wishes to protect. These pillars include health care, livelihood, education, and housing. We believe these areas will be or have already been subject to more regulation.

Health care may have been addressed in 2018, leading up to the new Five Year Plan. Education may have just been addressed, and livelihood, which involves antitrust and consumer protection enforcement, is currently underway, as evidenced by recent internet regulations. The real estate sector may be the next to field a period of heightened regulatory scrutiny as Xi Jinping stated at the 19th Party Congress that “housing is for living, not for speculation.”

China’s leaders made it abundantly clear in the 14th Five Year Plan, which will guide policy until 2025, that supporting the development of the digital economy is a policy priority4. New regulations on the internet sector are likely to promote the sustainable growth of internet platforms and are similar to policies implemented and introduced in both the U.S. and Europe, such as GDPR.

We believe the regulations thus far will enforce fair competition, resulting in better service that will benefit consumers. Furthermore, regulatory clarity in areas such as Fintech, which had been perceived as a potential systemic risk in China's financial system, should be welcomed. Clear rules for these industries may allow for increased transparency and sustainable growth.

The Restructuring of Online Education

Recent announcements regarding after-school tutoring (AST) regulations triggered massive selling in online education stocks and a panic plunge in the broader China markets. Online education stocks make up 1.17% of the CSI Overseas China Internet Index as of July 28th, 2021.5

While news of pending regulation on AST companies was widely telegraphed, the new rules were worse than what analysts anticipated. For-profit companies were banned from providing after-school tutoring programs for K-12 students. China's government believes that AST programs capitalized on parents' anxieties through aggressive advertising. According to the National Bureau of Statistics of China, after-school tutoring consumed over 20% of annual household expenditure in 20176. At the same time, recent census data in China revealed that population growth is well below desired levels. While the news has been painful for investors, China's government aims to reduce the financial costs of having children. Lowering apartment prices will likely be the government's next focus.

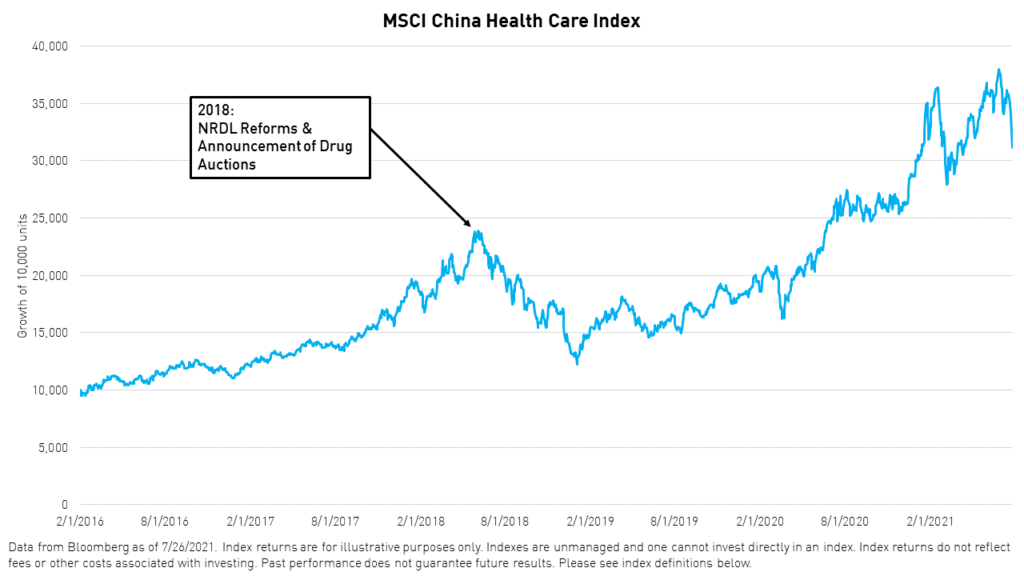

Parallels to Health Care in 2018

Recent reforms in China's health care sector may serve as a helpful guidepost for what could happen now in China's internet sector. From 2018 to 2019, the health care sector underwent a regulatory restructuring of some of its core industries. Systems were put in place to drastically reduce the cost of generic drugs through the reform of the Annual National Reimbursement Drug List (NRDL) and the establishment of a central procurement and auction system7. The reforms came at the detriment of China's generic drug-makers, and the near-term impact on stock prices in the sector was severe. The MSCI China Health Care index declined by 35% from May 31, 2018, to January 31, 2019.8

As the more positive impacts of reform started to take effect, the sector rebounded sharply, returning 104% from January 31, 2019, to July 26, 20219. Most importantly, reforms proved efficient and gave birth to a highly productive biotechnology industry, which currently boasts a robust pipeline of world-class innovative drugs.

Conclusion

We understand the fear and doubt mounting from international investors. The pace and scale with which recent reforms were introduced and implemented have been tremendous. However, China is no stranger to delivering such reforms. Earlier in the 1980s, the country's policies transformed rural areas spurring millions of people to move into cities, which created the largest middle class in the world. Investors have benefitted from these trends, especially investors in China's internet sector, which includes companies such as Tencent, which has achieved over 64,000% returns since going public in 2004.10

Furthermore, we see several near-term catalysts that could boost performance for the sector:

- Second-quarter earnings reports are coming, starting with Alibaba next Tuesday after market close in Hong Kong. The company may announce buybacks.

- As companies' market capitalizations near the same value of their cash reserves, we could see smaller companies buy back their public shares and go private.

- China's mainland A-shares reacted to regulatory concerns Monday and Tuesday for the first time. While mainland investors have considerable capital in Hong Kong, poor performance in the mainland could give regulators pause.

- The current massive valuation gap between China internet and U.S. internet is hard to ignore. China internet stocks are currently trading at around 16 times earnings, while US internet stocks are trading at around 42 times earnings, on average.11

We believe that sound, objective analysis of policy and economic events in China is more valuable than ever. Understanding what China shares with the U.S./Western World and what it does not is essential in making a well-informed decision regarding investing in China.

KraneShares hopes to serve as your trusted partner and guide through China's capital markets, driven by objective analysis.

Citations:

- "China launches 6-month campaign to clean up apps," Associated Press. July 26, 2021.

- National Bureau of Statistics of China as of 12/31/2020, retrieved 7/28/2021.

- Ministry of Industry and Information Technology release on 7/9/2021.

- 14th Five Year Plan (2021-2025).

- Data from KraneShares as of 7/28/2021.

- Data from National Bureau of Statistics of China as of 12/31/2018, retrieved 7/28/2021.

- "China to further reform centralized drug procurement system", Xinhua, 12/10/2019.

- Data from Bloomberg as of 7/26/2021.

- Data from Bloomberg as of 7/26/2021.

- Data from Bloomberg as of 7/26/2021.

- Data from Factset as of 7/27/2021. China internet stocks as represented by the CSI Overseas China Internet Index. US internet stocks as represented by the Dow Jones Internet Composite Index.

Definitions:

Price to Earnings (P/E): A valuation metric used by investors to gauge whether a stock is overpriced or underpriced. P/E is a ratio that divides the price per share by the earnings per share for a given company. The lower the ratio, the cheaper a stock is relative to earnings and vice versa.

Index Definitions:

MSCI China Health Care Index: The MSCI China Health Care Index captures large and mid-cap representation across China H shares, B shares, Red chips, and P chips. Currently, the index also includes Large Cap A shares represented at 10% of their free float-adjusted market capitalization. All securities in the index are classified in the Health Care sector as per the Global Industry Classification Standard (GICS®). The index was launched on January 1, 2001.

The CSI Overseas China Internet Index: CSI Overseas China Internet Index selects overseas-listed Chinese Internet companies as the index constituents; the index is weighted by free-float market cap. The index can measure the overall performance of overseas-listed Chinese Internet companies. The Index is within the scope of the IOSCO Assurance Report as of 30 September 2018. The index was launched on September 20, 2011.

Dow Jones Internet Composite Index: The Dow Jones Internet Composite Index is designed to measure the performance of the 40 largest and most actively traded stocks of U.S. companies in the internet industry. To be eligible for the index, a company must derive at least 50% of cash flows from the internet. The index was launched on February 18, 1999.